The travel credit card market has never been more competitive. Banks are fighting for your spending with bigger bonuses, richer category multipliers, and more valuable perks. That means better cards for everyone — but also more complexity in choosing.

This guide cuts through the noise. Whether you're opening your first travel card or building a multi-card setup, here are the six best travel credit cards of 2026 — and exactly who each one is built for.

How We Rank These Cards

Every card on this list was evaluated on five criteria: sign-up bonus value, ongoing earning rates, annual fee justification, transfer partner access, and strategic flexibility. We do not rank cards based on affiliate compensation or marketing partnerships.

One important note: the order you apply for these cards matters as much as which cards you choose. Chase's 5/24 rule means applying for too many cards too quickly can lock you out of the best Chase products. Before stacking cards, read our guide on credit card application order strategy.

1. Chase Sapphire Preferred — Best for Beginners

Annual fee: $95 | Welcome bonus: 60,000-100,000 UR points

The Chase Sapphire Preferred has been the entry point for serious points hackers for over a decade, and it earns that title in 2026. No card delivers more first-year value at this price point.

Earning rates: 5x on Chase Travel, 3x on dining and select streaming, 3x on online groceries, 2x on all other travel, 1x everything else. The 3x dining rate alone is competitive with cards costing twice the annual fee.

The real power is the ecosystem. Chase Ultimate Rewards transfers 1:1 to 14 airline and hotel partners including United MileagePlus, World of Hyatt, British Airways Avios, Air Canada Aeroplan, Air France/KLM Flying Blue, and Singapore KrisFlyer. For a deep breakdown of every partner and the best sweet spots, see our Chase Ultimate Rewards complete guide.

The sign-up bonus alone — typically 60,000 points, often elevated to 80,000-100,000 — is worth $900-$2,000 in travel when transferred to partners. That's 9-20 times the annual fee in year-one value.

Best for: Anyone opening their first or second travel card. The Preferred sits below Chase's 5/24 threshold on importance — get it early before accumulating too many cards.

Downgrade path: After two years, consider product-changing to the Chase Freedom Unlimited (no annual fee, still earns UR) if you add the Sapphire Reserve. This keeps your points earning without paying two Sapphire fees.

2. American Express Gold Card — Best for Foodies and Grocery Spenders

Annual fee: $325 | Welcome bonus: 60,000-100,000 Amex MR points

No card earns faster at restaurants and U.S. supermarkets than the Amex Gold. Period.

The earning rates: 4x at restaurants worldwide, 4x at U.S. supermarkets (up to $25,000/year), 3x on flights booked directly with airlines or via amextravel.com, 1x everywhere else. If your household spends $2,000/month on food — dining out plus groceries — you're earning 8,000+ Amex MR points per month from those two categories alone.

The annual fee is $325, but between the $120 dining credit (Grubhub, Cheesecake Factory, Goldbelly, Wine.com, Five Guys), $120 Uber Cash credit, and $100 Resy credit, there's $340 in credits available — meaning the card effectively pays you $15 per year if you use the credits.

Amex Membership Rewards transfers to 20+ partners including Delta SkyMiles, Air France/KLM Flying Blue, ANA Mileage Club, Singapore KrisFlyer, Virgin Atlantic Flying Club, and Marriott Bonvoy. The full transfer partner breakdown is in our Amex Membership Rewards complete guide.

Best for: High grocery and restaurant spenders. Pairs exceptionally well with the Chase Sapphire Preferred — Chase for travel, Amex Gold for food — covering nearly every spending category at 3x-4x.

Player 2 strategy: Adding an authorized user to the Amex Gold earns a separate referral bonus and lets a partner earn Amex MR on their spending. Since Amex MR points pool across household members, this effectively doubles your earning rate without opening a second card account.

3. Capital One Venture X — Best Premium Card Value

Annual fee: $395 | Welcome bonus: 75,000 miles

The Venture X punches far above its $395 annual fee — a fee that's effectively $0 if you use the travel credit and anniversary bonus.

Here's the math: the card comes with a $300 annual travel credit (applied to Capital One Travel bookings) and a 10,000-mile anniversary bonus worth roughly $100. That's $400 in recurring annual value against a $395 fee. You're netting positive before you earn a single mile from spending.

Earning rates: 10x on hotels and rental cars via Capital One Travel, 5x on flights via Capital One Travel, 2x on everything else. The unlimited 2x base rate is the highest of any no-category-limit premium card. Every dollar you spend earns at least 2 miles.

Capital One Miles transfer to 17+ airline and hotel partners at mostly 1:1 ratios, including Turkish Airlines Miles&Smiles, Avianca LifeMiles, Air France/KLM Flying Blue, Singapore KrisFlyer, and Wyndham Rewards. Turkish and Avianca offer some of the best premium cabin sweet spots available — United Polaris to Europe for 45,000-60,000 miles, Lufthansa First for 87,000 miles.

Cardholders also get Priority Pass Select membership with unlimited lounge visits, Capital One lounge access (a growing network), and Hertz President's Circle status.

Best for: Travelers who want one premium card without the complexity of managing multiple high-fee cards. The Venture X is the most straightforward path to lounge access and premium perks.

4. Citi Strata Premier — Best Category Multipliers Under $100

Annual fee: $95 | Welcome bonus: 60,000-75,000 ThankYou Points

The Citi Strata Premier is the most underrated card in this roundup. For $95 a year, you get 3x on hotels, air travel, restaurants, supermarkets, gas stations, and EV charging — covering virtually every major spending category at 3x.

Most cards require you to buy into a $500+ annual fee product to get 3x on hotels. The Strata Premier gives you that rate plus dining, groceries, and gas for $95. For moderate spenders, this is genuinely one of the best earning cards available regardless of fee tier.

Citi ThankYou Points transfer to 16 partners including American Airlines AAdvantage (the only major transferable currency with direct AA access), Turkish Miles&Smiles, Singapore KrisFlyer, Air France/KLM Flying Blue, and Choice Hotels (at a 1:2 ratio). The American Airlines transfer is uniquely valuable — AA's partner award chart still has fixed pricing with Qatar Qsuites at 70,000 miles one-way, JAL First at 80,000 miles, and no fuel surcharges.

Best for: The second or third card in a portfolio, especially if you do not have American Airlines transfer access elsewhere. Also excellent as the primary card for someone who maxed out their Amex Gold's grocery cap.

Application timing note: Citi enforces an 8/65 rule — no more than one card per 8 days and two cards in 65 days. Apply for the Strata Premier during a window when you have not recently opened other Citi products.

5. Bilt Mastercard — Best for Renters (No Annual Fee)

Annual fee: $0 | Welcome bonus: None (variable Rent Day offers)

The Bilt Mastercard solves a problem every renter faces: rent is your largest monthly expense and most cards charge a fee to pay it — eating your rewards before you earn them.

Bilt lets you pay rent on any rental property with no transaction fee. You earn 1x Bilt Rewards on rent (up to 100,000 points per year), 3x on dining, 2x on travel, and 1x on everything else. With the average U.S. rent at $1,700/month, that's 20,400 free Bilt points annually just from your rent payment.

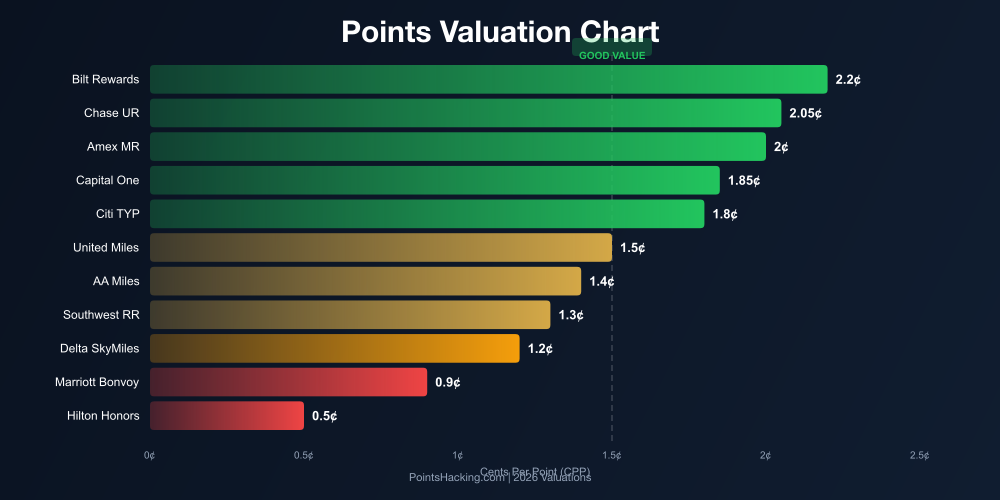

Bilt Rewards transfers to 20 partners and carries the highest per-point valuation of any program at roughly 2.2 cents per point (per The Points Guy). The exclusive access to Alaska Mileage Plan (rebranded Atmos) — not accessible via Chase, Amex, Capital One, or Citi — unlocks Cathay Pacific First at 70,000 miles, JAL First at 70,000 miles, and Emirates First at 100,000 miles with no fuel surcharges.

The Rent Day promotion (first of each month) offers 1x bonus points on all purchases plus occasional 100%+ transfer bonuses to select partners. Hitting Bilt Platinum status (by spending at a set threshold) unlocks bonus points on Rent Day purchases.

Best for: Any renter. This is the only card that turns your rent into premium travel. The no-annual-fee structure and Alaska access make it a must-have regardless of your other cards.

Important rule: You must make at least 5 transactions per statement period for your points to post. Bilt requires activity — use the card for at least five small purchases each month.

6. Chase Freedom Unlimited — Best No-Fee Earning Card

Annual fee: $0 | Welcome bonus: Variable (sometimes $200 cash back)

The Freedom Unlimited earns 1.5x Chase Ultimate Rewards on all purchases, 3x on dining and drugstores, and 5x on Chase Travel. Alone, those points redeem for 1 cent each as cash back. Paired with a Sapphire Preferred or Reserve, they unlock full transfer partner access at a higher portal redemption rate.

This is the "points vault" card — the no-fee product you keep after downgrading your Sapphire Preferred or as a permanent spending card for everything that does not hit a bonus category. Every dollar spent earns at least 1.5x versus the standard 1x on most cards, and all those points feed into your Chase UR balance for transfer partner redemptions.

Best for: Anyone in the Chase ecosystem who wants to maximize every-day non-category spending without paying a second annual fee. Pair it with the Sapphire Preferred and the Chase Ink Business Cash for one of the strongest three-card no-overlap setups available.

Beginner vs. Advanced Card Strategy

If you are just starting (0-2 cards): Open the Chase Sapphire Preferred first. Add the Bilt Mastercard if you rent. That two-card setup covers travel, dining, groceries, and rent with excellent transfer partner access — without complexity or high annual fees.

If you are building a portfolio (3-5 cards): Add the Amex Gold for food spending after establishing your Chase cards. Consider the Citi Strata Premier for American Airlines access. Keep a no-fee card in each ecosystem (Freedom Unlimited, Blue Business Plus, Citi Double Cash) to maintain points-earning without annual fees.

If you are optimizing (5+ cards): The Venture X may replace or complement the Sapphire Reserve as your premium travel card. Business cards (Ink Business Preferred, Amex Business Gold) open a second application track outside the 5/24 rule and carry some of the largest welcome bonuses available. The application order and timing for this phase is covered in our credit card application order strategy guide.

The Player 2 Strategy

If you have a partner or spouse, your card strategy doubles. The simplest version: one person focuses on Chase cards, the other on Amex. Both earn the respective sign-up bonuses. Both transfer to the same shared award accounts (most airlines allow family pooling).

The more advanced version: both people follow the same optimal card order but on a 6-12 month offset. Person 1 opens Sapphire Preferred in January. Person 2 opens Sapphire Preferred in July. Combined, you collect two sign-up bonuses. You get authorized user cards on each other's accounts to consolidate points.

Authorized user strategy also matters for keeping points alive. Amex MR points stay alive as long as you have one MR-earning card open. Chase UR points evaporate if you close all Chase cards — keep the Freedom Unlimited as a permanent no-fee vault to prevent that.

For more on how banks like NerdWallet and other review sites evaluate these cards against competitors not covered here, see NerdWallet's full travel card rankings.

Annual Fee Analysis: When Premium Cards Pay Off

Premium cards like the Amex Platinum ($695) and Chase Sapphire Reserve ($550) carry fees that require active use to justify. The math only works if you use the credits. The Amex Platinum's $200 airline fee credit, $200 hotel credit, $240 digital entertainment credit, and $155 Walmart+ credit add up to $795+ in potential value — but only for people who would use those specific services.

Rule of thumb: never pay a premium annual fee if you cannot realistically use at least 80% of the credits in the first year. The Amex Gold and Chase Sapphire Preferred deliver better effective value for most people precisely because their credits (dining, Uber, travel) are universally applicable.

The sign-up bonus is not a reason to ignore annual fee math. A 100,000-point bonus worth $1,500 is excellent in year one. But in year two, you need the ongoing benefits to justify renewal. Evaluate every card at the 11-month mark before the next annual fee posts.