Most people think about credit cards one at a time. Find a good card, apply, earn the bonus, repeat. That approach leaves thousands of dollars in sign-up bonus value on the table — and can lock you out of the best cards entirely.

The order you apply for credit cards is a strategic decision. Get it wrong and you might hit Chase's 5/24 wall with half your planned cards still unobtained. Get it right and you systematically unlock every major card program in the optimal sequence with no restrictions blocking you.

This guide covers the exact application order strategy used by serious points hackers — from the rules that govern each bank to the spacing between applications to hard pull management.

Why Order Matters: The 5/24 Problem

Chase enforces a rule called 5/24: if you have opened 5 or more new credit cards in the past 24 months (from any bank, not just Chase), Chase will automatically deny your application for most of their cards.

This is the defining constraint of any multi-card strategy. Chase has some of the best travel cards available — the Sapphire Preferred, Sapphire Reserve, Ink Business Preferred, Ink Business Cash — and they are the most time-sensitive to obtain.

If you open five non-Chase cards first, you lose access to the Chase ecosystem for potentially years. That means forgoing sign-up bonuses worth $1,000-$2,500 per card.

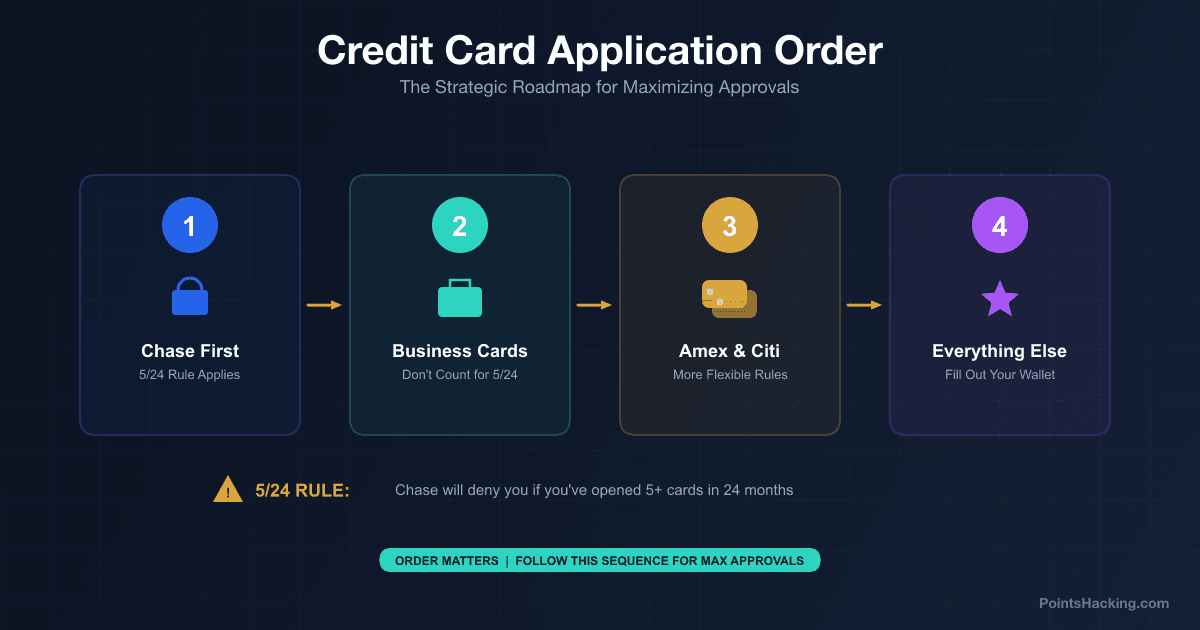

The strategy: Chase first. Always.

Before you apply for any Amex, Capital One, Citi, or other card, lock in every Chase card you want. Only then move to other issuers. For the full breakdown of which Chase cards are worth prioritizing, see our best travel credit cards of 2026 guide.

Phase 1: Chase Personal and Business Cards

Your Chase phase should include every Chase card you want before you go anywhere else. The priority order within Chase:

1. Chase Sapphire Preferred or Reserve — Your foundational Chase card. The Sapphire products are subject to 48-month bonus restrictions (you can only earn the Sapphire bonus once every 48 months across Preferred and Reserve combined). Get one early.

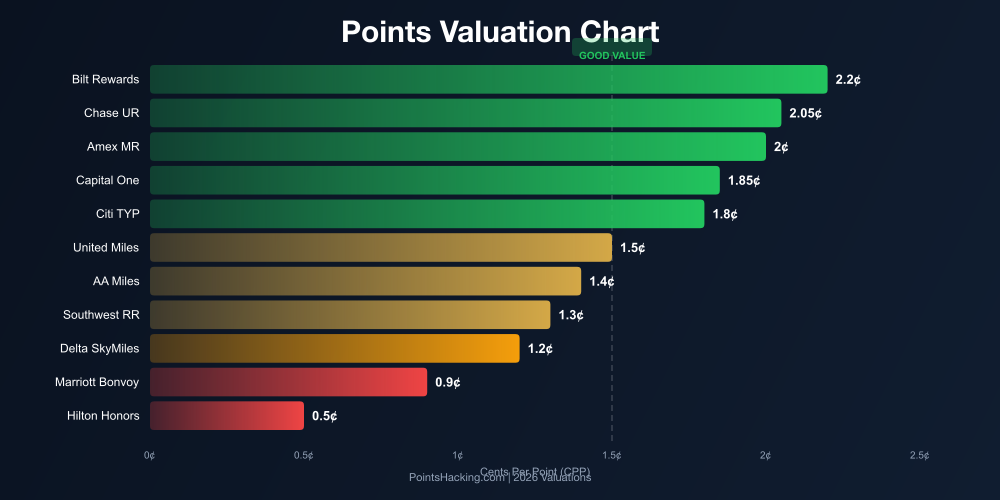

2. Ink Business Preferred, Ink Business Cash, Ink Business Unlimited — Business cards do not count toward your personal 5/24 count when you hold them (though applying adds a hard pull). The Ink suite earns massive Chase UR — the Ink Business Preferred offers 100,000 UR bonus points, one of the largest available bonuses of any card.

Important: you do not need a registered LLC or corporation to apply for business cards. Sole proprietorships qualify. If you sell anything, freelance, or have any self-employment income, you have a qualifying business. Use your SSN as the EIN and your name as the business name.

3. Chase Freedom Unlimited and/or Freedom Flex — No-fee cards that earn 1.5x-5x UR and serve as permanent points vaults. Apply for these in Phase 1 so you have no-fee UR-earning cards locked in before you potentially hit 5/24 from other issuers.

Recommended spacing within the Chase phase: one card every 30-90 days. Chase gets nervous about rapid applications and may flag your account for review. Waiting 90 days between Chase cards is conservative but optimal. Waiting 30 days is the minimum to avoid automatic shutdown review.

Phase 2: Non-Chase Business Cards

After you have your Chase personal cards secured, shift to non-Chase business cards. Business cards from Amex, Capital One, and Citi generally do not appear on your personal credit report and do not count toward Chase 5/24.

This means you can collect large sign-up bonuses without eroding your Chase eligibility. The best non-Chase business cards:

Amex Business Gold: 4x on the two categories you spend most in each month (from a list including advertising, technology, restaurants, gas, and shipping). Welcome bonus of 100,000-150,000 MR points.

Amex Business Platinum: 5x on flights and hotels booked through Amex Travel, 1.5x on purchases over $5,000. Welcome bonus of 150,000-200,000 MR points — the largest in the points ecosystem. $695 annual fee requires credit use to justify.

Capital One Venture X Business: 10x on hotels and car rentals, 5x on flights, 2x on everything else. Does not count toward personal 5/24.

Space business cards 90+ days apart to manage hard pull velocity and avoid simultaneous credit review flags.

Phase 3: Non-Chase Personal Cards

Once you have maximized the Chase ecosystem and loaded up on non-Chase business cards, you can finally open personal cards from other issuers — even if those applications push you over 5/24. At this point, you have already captured the Chase value and 5/24 no longer constrains you.

Priority order for Phase 3 personal cards:

Amex Gold — 4x dining and groceries, Amex MR ecosystem access. The most popular Phase 3 first move for foodies.

Citi Strata Premier — 3x on virtually everything, including American Airlines transfer access. See the Chase Ultimate Rewards complete guide for how UR compares to Citi ThankYou access.

Capital One Venture X — If you did not get the business version, the personal card unlocks the same transfer partner network plus a $300 annual travel credit.

Bilt Mastercard — No annual fee, earns on rent. Can actually be opened in Phase 1 or early Phase 2 since it typically does not count against 5/24 (it is a Mastercard issued by Wells Fargo, which has no bonus frequency restrictions).

Application Rules by Bank

Every major issuer has its own rules governing how often you can apply and earn bonuses. Violating these rules means denied applications, clawed-back bonuses, or closed accounts.

Chase Rules

5/24: 5 or more new cards in 24 months = automatic denial on most Chase cards. Business cards you hold do not add to the count, but the hard inquiry from applying still appears.

2/30: Chase will not approve more than 2 personal cards within any 30-day period. Some data points suggest 1/30 is safer for most applicants.

Sapphire 48-month rule: You can only earn the Sapphire (Preferred or Reserve) bonus once every 48 months. If you had the Preferred, wait 48 months from the date you received the bonus before applying for either Sapphire again.

Ink velocity: Chase has become more restrictive with Ink business cards in 2025-2026. Many applicants find approval easier with 90+ days between Ink applications and total Ink cards below 4-5.

Amex Rules

Once per lifetime: The most important Amex rule. You can only earn the welcome bonus on any given Amex card once in your lifetime. If you had the Amex Gold three years ago and closed it, you will not receive the welcome bonus if you reopen it. This applies per card product, not per issuer.

This makes Amex card selection critical. Do not open an Amex card until you are confident you want it and will earn maximum value from the bonus. The welcome offer varies — apply during a targeted or elevated offer, not at the standard offer.

2/90: Amex will not approve more than 2 cards in any 90-day period across personal and business.

5 card max: Amex limits you to 5 credit cards (not charge cards) at once. Charge cards like the Amex Platinum and Gold have no stated limit (though practical limits apply).

No hard pull guarantee: Amex sometimes lets you check for pre-approval without a hard pull. Check your Amex pre-approval offers before applying cold to minimize unnecessary hard inquiries.

Citi Rules

8/65: No more than one Citi card per 8 days, and no more than two cards in 65 days. This is a hard cutoff — apply on day 8 or later after your last Citi card application.

24/48 month bonus rule: Citi enforces bonus eligibility based on when you opened or closed the same card family. For the Strata Premier (formerly Premier), you cannot earn the bonus if you received a bonus from the same card family in the past 24 months, or if you currently hold or closed a card in that family within 24 months. Check before applying.

Capital One Rules

6-month rule: Capital One typically wants 6 months between applications. Some data points suggest they pull from all three credit bureaus (Experian, Equifax, and TransUnion) — three hard pulls per application, which is uniquely aggressive among issuers.

2 card max: Capital One limits you to 2 personal cards open simultaneously. If you have 2 Capital One personal cards and want another, you must close one first.

Because Capital One pulls three bureaus, many experienced applicants save Capital One applications for windows when they have no other applications planned — minimizing total hard inquiry accumulation.

Hard Pull Management

Each credit card application triggers a hard inquiry on your credit report. Multiple hard inquiries in a short window can meaningfully lower your credit score (typically 5-10 points per inquiry) and signal risk to banks reviewing your file.

Best practices for managing hard inquiries:

Space applications 30-90 days apart — 30 days is the minimum for most banks. 90 days is conservative but substantially reduces risk of adverse action.

Track all inquiries in a spreadsheet — Log every application with the date, issuer, result, and which bureau was pulled. This prevents accidentally applying during restriction windows.

Know your bureaus — Chase typically pulls Experian (sometimes TransUnion). Amex usually pulls Experian. Capital One pulls all three. Citi pulls Equifax or Experian depending on region. Applying for a Chase and Amex card on the same day generates two Experian pulls — acceptable but not ideal.

Protect your 5/24 count — Check your 5/24 status before any application by reviewing new accounts in your TransUnion or Experian report. Count all personal cards opened in the last 24 months. Store cards, authorized user accounts (sometimes), and most business cards do not count.

Recommended Spacing Between Applications

General spacing framework:

- Chase to Chase: 90 days minimum (30 days absolute minimum)

- Chase to non-Chase: 30 days (Chase inquiry needs time to age)

- Amex to Amex: 90 days (2/90 rule enforcement)

- Citi to Citi: 65 days (8/65 rule)

- Capital One to Capital One: 6 months

- Capital One to anything else: 30 days minimum (3-bureau pull needs time to age)

The best external resource for tracking bank-specific data points and rules updates is Doctor of Credit, which aggregates real-time reports from applicants and maintains the most accurate bank rule database available.

Putting It Together

The application order strategy is most powerful when combined with knowledge of which cards to prioritize in each phase. For Amex specifically, the once-per-lifetime bonus rule means sequencing matters — you want to apply for Amex cards in order of highest bonus first, and never apply without a targeted offer. Our Amex Membership Rewards complete guide covers exactly which cards to prioritize and which bonuses to wait for.

For Chase, the Ink Business card series represents some of the best total bonus value available. Getting three Ink cards — Ink Preferred, Ink Cash, and Ink Unlimited — at 90-day intervals can yield 200,000-400,000 Chase UR points depending on current bonus levels. That is $3,000-$8,000 in travel value from business card bonuses alone, accessible even after you are over 5/24.